FICO Credit Scores

Millennials are now ages 18 to 36, and while they have pushed off entering the housing market longer than other generations, they are now moving towards settling down. According to Kelsey Ramirez at Housingwire, “Their FICO credit scores are improving as well as more Millennials move toward conventional loans, and away from FHA-backed loans, bringing the average FICO score for Millennial borrowers up slightly, according to Ellie Mae, a provider of software solutions and services for the residential mortgage industry.”

Millennials are now ages 18 to 36, and while they have pushed off entering the housing market longer than other generations, they are now moving towards settling down. According to Kelsey Ramirez at Housingwire, “Their FICO credit scores are improving as well as more Millennials move toward conventional loans, and away from FHA-backed loans, bringing the average FICO score for Millennial borrowers up slightly, according to Ellie Mae, a provider of software solutions and services for the residential mortgage industry.”

What are FICO credit scores? Caroline Mayer, consumer blogger says, “It’s an algorithm designed to predict your likelihood of repaying debt. Lenders use your score to determine whether to approve you for loans and credit cards and at what interest rates. Insurers use credit scores to set premium rates, and employers use them when making hiring decisions.

FICO credit scores run from 300, considered the highest risk of default, to 850, the lowest risk. Though FHA for years has accepted applicants who have FICO scores in the 500s, the practical reality has been that most lenders ignore borrowers whose scores are under 620 or even 640.

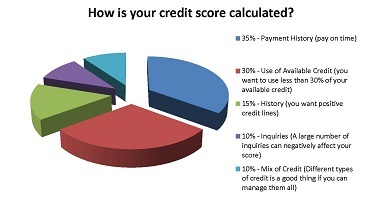

How are FICO credit scores calculated? Here is Cedar Rapids, your score is based on many different pieces of credit data in your credit report. This data is grouped into five categories as outlined below. The percentages in the chart (above) reflect how important each of the categories is in determining how your FICO Scores are calculated.

If you don’t know your FICO credit score, you can request a free copy of your credit report then check it for errors, such as late payments incorrectly listed for any of your accounts and that the amounts owed for each of your open accounts is correct. If you find errors on any of your reports, dispute them with the credit bureau.

Forbes says to be careful with some consumer sites offering free credit reports. “The new free scores from consumer sites are often “ballparks,” not the ones used by financial institutions to determine credit. Even more confusing, your FICO credit score or Vantage score may differ from lender to lender, since each institution can tinker with the parameters.

Some use scores created by FICO. Others use VantageScore, developed by credit rating bureaus Experian, Equifax and TransUnion. Still others compute scores by working with a single credit bureau. FICO and TransUnion’s New Account Score ranges from 300 to 850; Vantage, from 501 to 990; Equifax’s is between 280 and 850 and Experian is 330 to 830.

Kenneth Harney at The Real Deal writes, “If you’ve got a low FICO credit score but believe you can handle monthly mortgage payments instead of rent, here’s some potentially good news: The government is now willing to give you a better shot at obtaining a low-down-payment home loan from the Federal Housing Administration. Under a key policy change that took recently, lenders nationwide now have more leeway to approve mortgages to borrowers who qualify under FHA’s underwriting guidelines but may have below-par FICO credit scores.”

Got a Low FICO Credit Score?

Making your credit payments on time is one of the biggest contributing factors to your FICO credit scores. Set up reminders for making payments or switch from paying by check to automatic bank debits to each creditor.

Get out of debt. Reducing the amount that you owe is going to be a far more satisfying achievement than improving your credit score. The first thing you need to do is stop using your credit cards. Then come up with a payment plan that pays off the cards. Once credit card debt is gone, build an emergency fund equal to six months living expenses. Finally, save large amounts of money going to interest by paying off your mortgage early.

If you are ready to make the leap to owning a home and you have a low FICO credit score, shop around. You may get turned down by some lenders because they haven’t reduced their standards yet. Keep shopping until you find one that has. You are likely to find a better reception than you expected.

The best advice for rebuilding credit is to manage it responsibly over time. If you haven’t done that, then you need to repair your credit history before you see credit score improvement.

Harmony Property Solutions, LLC is here to help homeowners out of any kind of distressed situation. As investors, we are in business to make a modest profit on any deal, however we can help homeowners out of just about any situation, no matter what! There are no fees, upfront costs, commissions, or anything else. Just the simple honest truth about your home and how we can help you sell it fast to resolve any situation.

Harmony Property Solutions, LLC is part of a nationwide group of thousands of investors who are helping tens of thousands of homeowners every year. We may not be the “traditional” route, but we CAN help and we can do it quickly!

Give us a call today at 319-343-6773 to let us know what YOU need help with!